Picture Post Week: Subprime Chartering

A short while back, I explained how, in our fervor to rapidly expand charter schooling and decrease the role of large urban school districts in serving their resident school-aged populations, we’ve created some particularly ludicrous scenarios whereby, for example – charter school operators use public tax dollars to buy land and facilities that were originally purchased with other public dollars… and at the end of it all, the assets are in private hands! Even more ludicrous is that the second purchase incurred numerous fees and administrative expenses, and the debt associated with that second purchase likely came with a relatively high interest rate because – well – revenue bonds paid for by charter school lease payments are risky. Or so the rating agencies say.

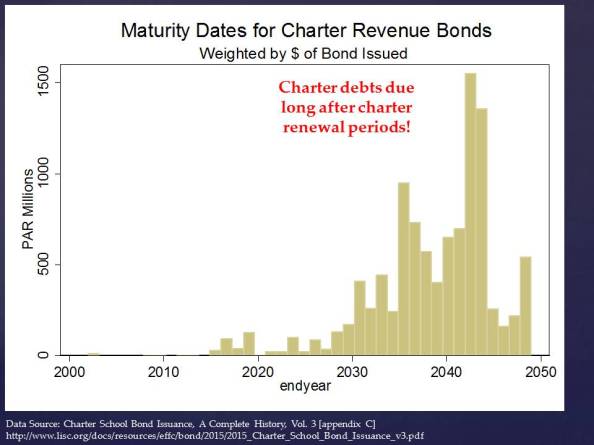

So how much of this debt is accumulating? And when does it come due? Who is issuing this debt? Are we looking at a charter school subprime bubble? Here are some snapshots:

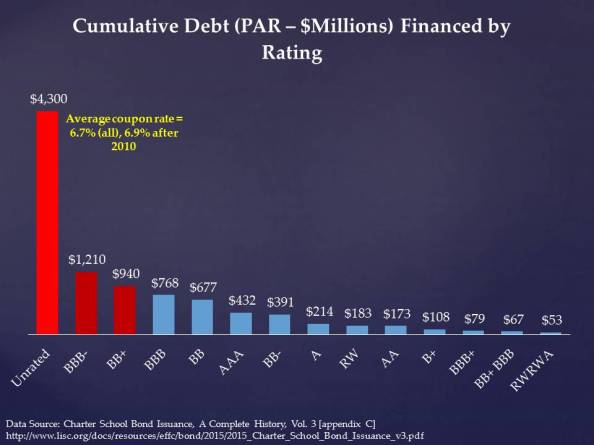

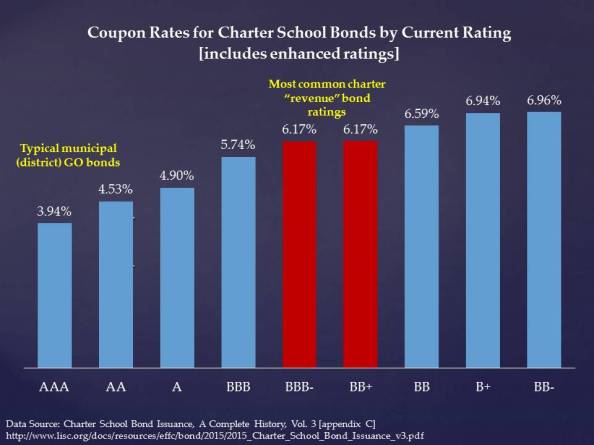

Most revenue bond debt incurred on behalf of charter schools is either unrated, or BBB- or BB+ rated. The unrated debt is saddled, on average, with coupon rates around 6.9% in recent years, marginally higher than rates attached to BBB- or BB+ bonds.